Lessons learnt from Germany’s mixed price system

Jan de Decker, Paul Kreutzkamp and Elias de Keyser from Next Kraftwerke Belgium explain in this blog what lessons can be learnt from the roughly nine months of the mixed price system on the reserve power market in Germany.

On July 22nd 2019, the Higher Regional Court of Dusseldorf decided to overturn the mixed price system in the German balancing markets that was in place since the fall of 2018. In this blogpost, we explain how the mixed price system led to a persistent upward trend in capacity prices for reserve power and a staggering amount of interventions of the German grid operators to keep the system in check. We as experts from Next Kraftwerke Belgium analyze the situation, explain the impact of the mixed price system and compare it with the Belgian market. Could we face similar problems over here? What does a healthy balancing market design look like? Continue reading to find out!

The firefighters of the electricity grid

A healthy grid is a balanced grid. However, since market parties base their exchanges in the electricity markets on forecasts and schedules, that balance is usually somewhat off. The reasons can be manifold: power consumption at a factory could be lower than expected, or an offshore wind farm could have more wind coming in, to name a few.

Network operators such as Elia are always on guard to restore the balance and ensure a stable and secure supply of electricity. To this end, they contract reserve capacity from market parties in order to cope with shortages and surpluses in the electricity network in real-time. This usually happens in two consecutive markets: the reserve capacity market, and the reserve energy market.

The first is meant to secure a given amount of power in advance to have it at the grid operator’s disposal in time of need. The selected providers receive a capacity remuneration and in return they are obliged to keep the awarded MW available. These costs are paid back via the grid tariffs and hence equally borne by all end consumers. Just like everyone pays the fire brigade to be on stand-by 24/7.

Next, the reserve energy market takes place. Here, the selected reserve power providers submit a price per MWh that would potentially be activated. In case of need, the grid operator will activate these bids starting at the cheapest. Only activated market parties receive the energy remuneration. On top, these costs are not borne by all end consumers, but charged through to the parties that caused the imbalance in the first place (this is known as the imbalance price). It gives a direct incentive to all balancing responsible parties to do their job as good as possible.

The old (and new) German System

Until October 2018 and from the 25th of July 2019 on, secondary and tertiary reserves are auctioned in an efficient and cost-effective manner. First, capacity is awarded in the capacity tender, open to market parties large and small such that a healthy competition determined the prices. Next, energy bids are activated following the merit order.

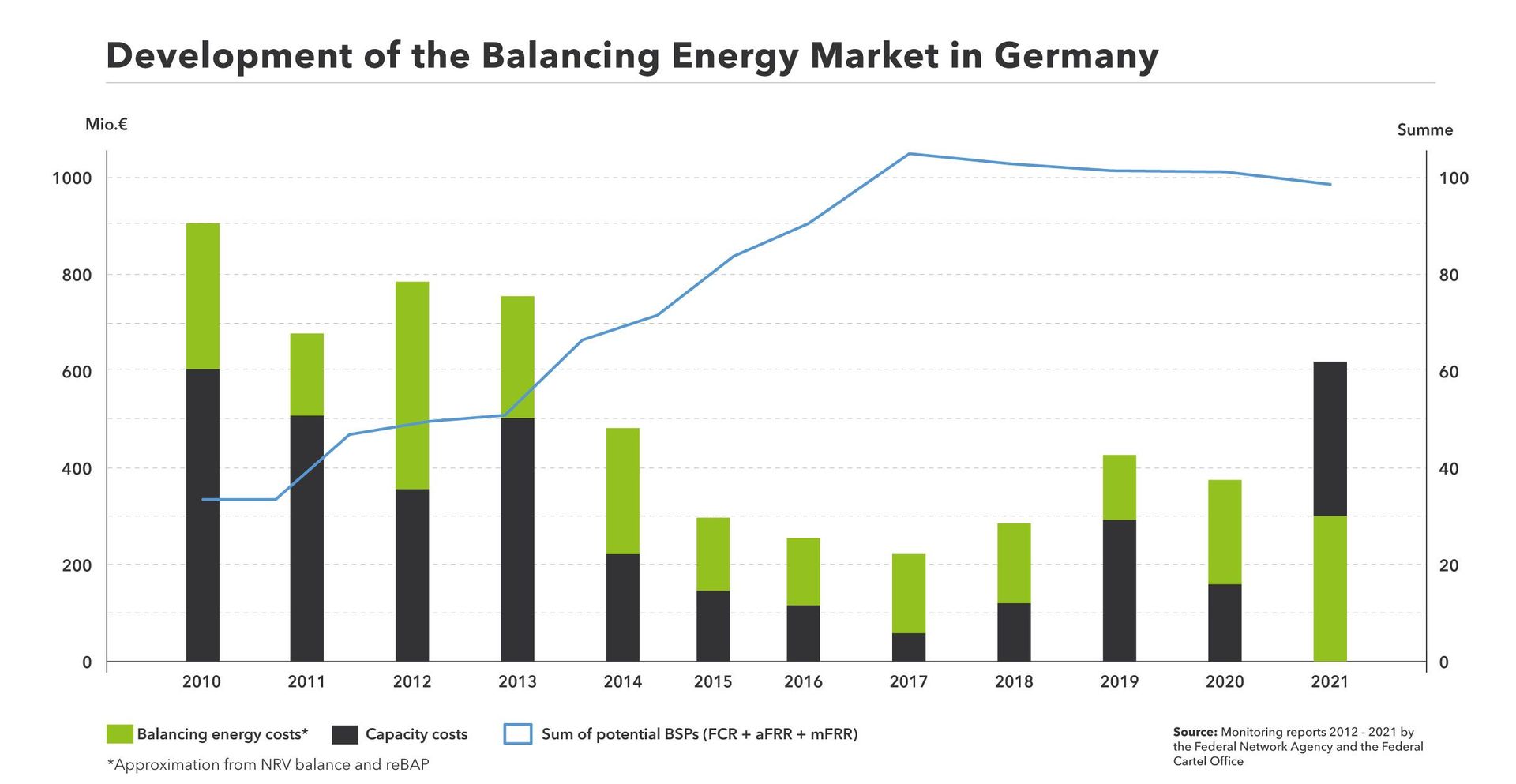

This approach led to one of the most competitive reserve power markets in Europe and, consequently, to very liquid power exchanges. The reservation costs for secondary and tertiary reserves were dropping year after year. At the same time, the absence of a price cap on energy bids meant that imbalance fees could be high for parties that managed their portfolio uncarefully. Traders therefore made sure to trade away foreseen excesses or shortages in the intraday market, to avoid an imbalance penalty altogether. As a result, the number of reserve power activations dropped significantly, while the volume traded intraday was never so high. This trend is illustrated in the graph below.

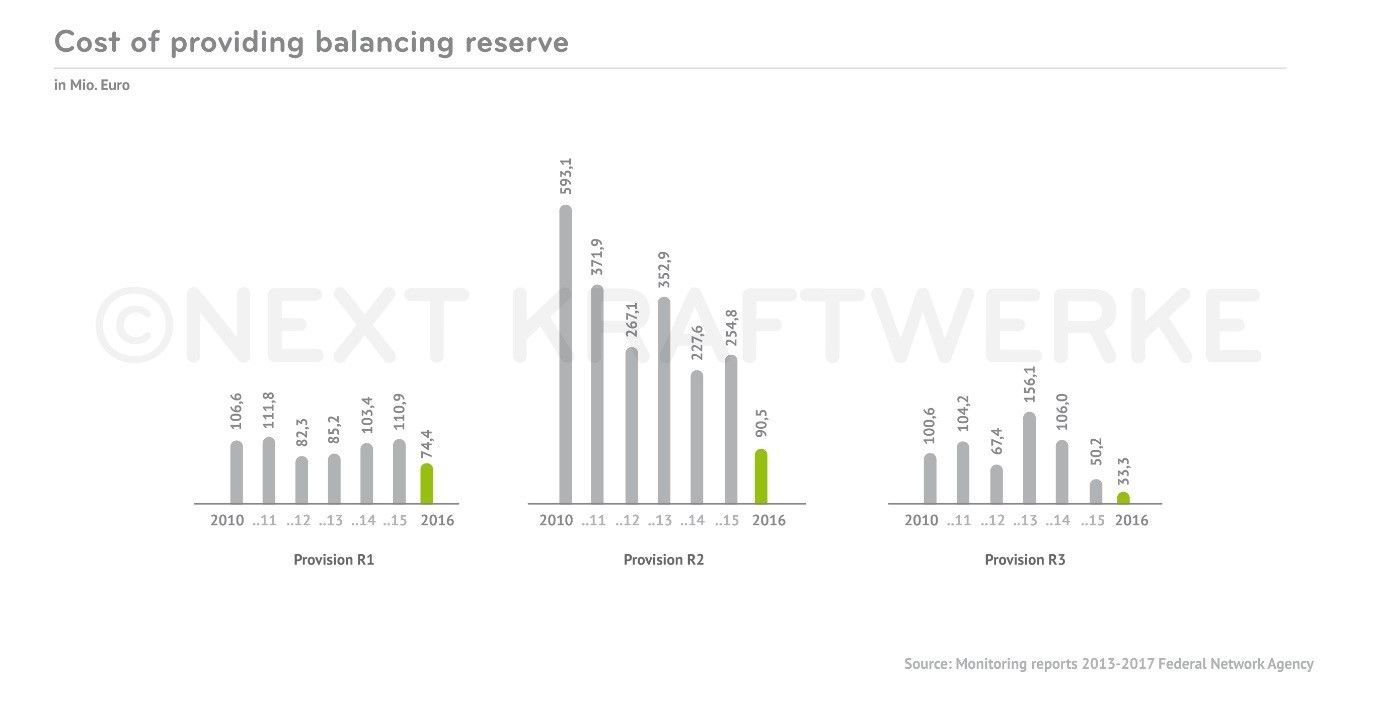

In short, the reservation costs plunged, and with them the costs for system balancing. At the same time, balancing parties managed assets to their best extent so that the grid operator needed to activate the reserve power less and less often. Society was better off with a cheaper and safer electricity system. The decrease of reservation costs of the three balancing products are shown in the graph below.

Where did it go wrong?

By now you must be wondering why the German Regulator decided to abandon this well-functioning approach in October 2018.

As always, where there are winners (in this case: society), there are losers. Not everybody might have been happy with the developments. Some market parties might have good reasons to long for the past, where capacity prices were high and activation prices low.

Was it such a party that wanted to stir things up by bidding an activation price of 77 777.77 euros per MWh on the 17th of October 2017? We still don’t know until this day… and we might never do. But we do know that the bid in question got activated that day by the grid operator to resolve a shortage in the grid, resulting in an unseen activation and imbalance price of 77 777.77 euros per MWh. With all consequences for parties that were in imbalance at that time.

It is also a fact that it triggered the German National Regulator for Electricity (the Bundesnetzagentur) to overthrow the German existing reserve power market design and install a mixed price system.

It is understandable that the prices in October 2017 were followed by political discussions and that the Regulator wanted to restrain imbalance prices to a certain extent. But the mixed price system seems to have been a bad choice. It makes market manipulations possible, but most importantly it undid many of the achievements of the existing market design.

The mixed price system

In the mixed price system, called Mischpreisverfahren in German, the selection of providers of reserve power is based on a mix of their capacity and energy bid. Instead of awarding the reserve power bids solely based on the capacity bid, it now takes into account the activation price bid to a certain extent. This coupling has drastically changed the dynamics of the balancing market.

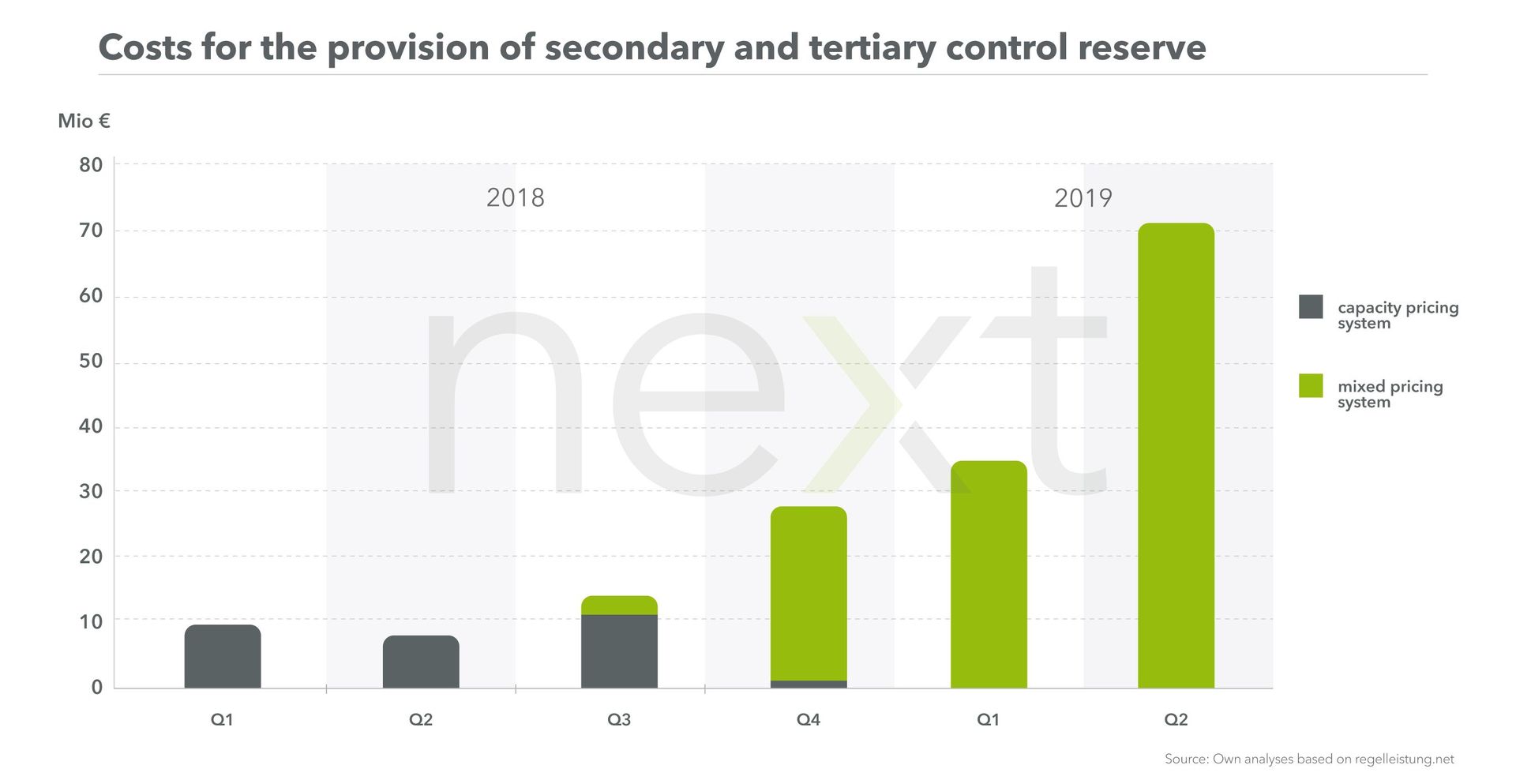

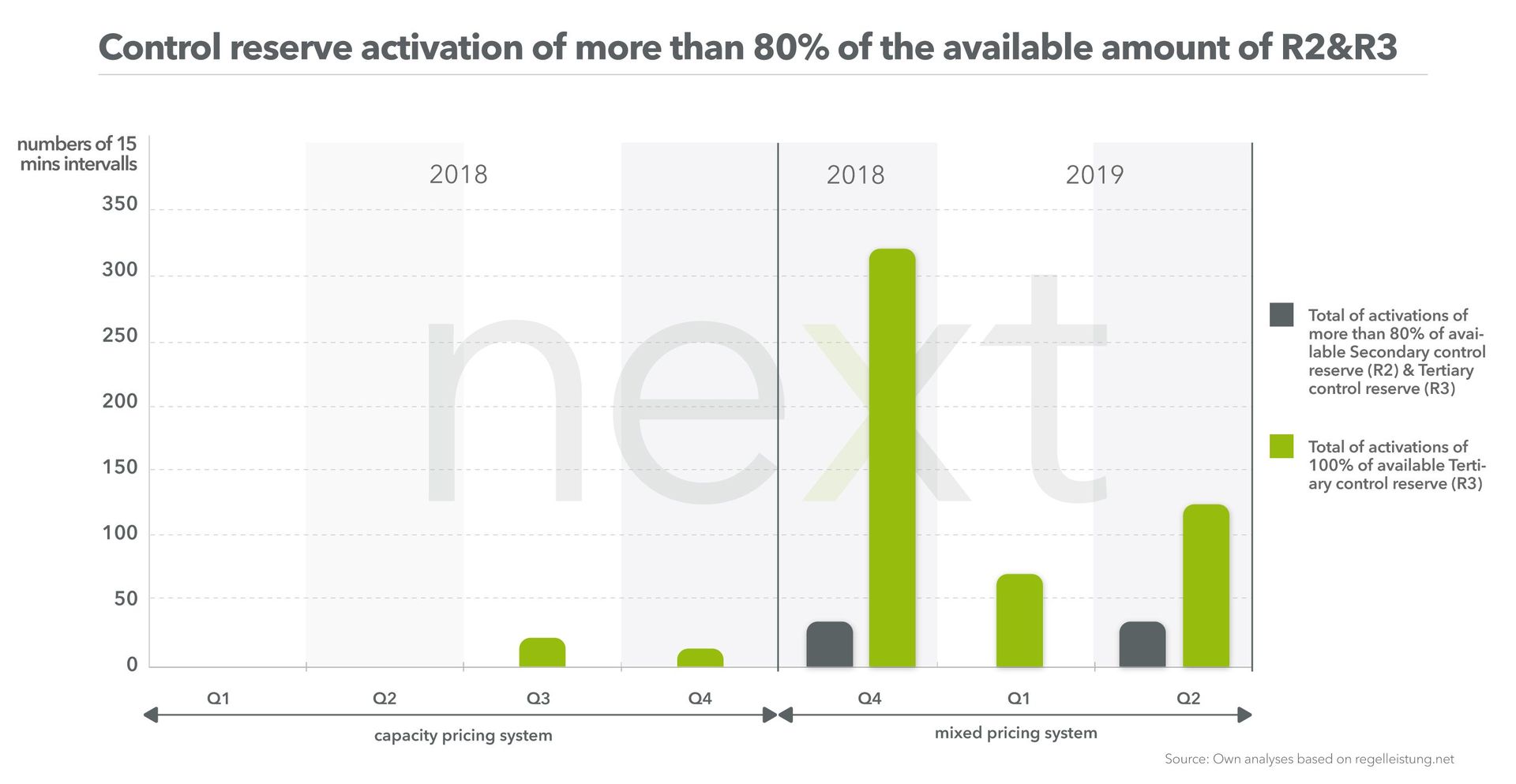

Since its introduction in October 2018, reservation prices have gone up dramatically (see the illustration below), while activation prices have dropped. The result is that end consumers pay for expensive assets to be kept available, while the costs for an actual intervention, paid by the parties who caused the imbalance, are reduced. As a consequence, such parties have little incentive anymore to invest in performant forecasting and are less eager to trade away imbalances on the intraday market.

Thus, the number of activations of reserve power have consequently increased again. Over the last few months, the grid operators exhausted several times most or all of their available reserve power. This led the German TSOs to increase the contracted volume of tertiary reserve. It looks like some market parties used this opportunity to drive up their capacity bids even further.

On Saturday the 29th of June, between 12 and 4PM, one market party offered and was awarded 92 MW tertiary reserve at the staggering reservation price of 37 856 euros per MW. Normally, the tertiary reserve price lies below 10 euros per MW. In four hours’ time, the reserve power provider in question earned 3.5 million euros.

In a sense, this reservation price is more remarkable than the activation price noted in October 2017. In the end, the latter was paid for by parties who caused the imbalance, while the first is paid by all grid users regardless of the fact that the reserve was activated or not.

Yet, in the morning of the 22nd of July 2019, the Higher Regional Court in Dusseldorf decided to overturn the mixed price procedure in a lawsuit against the German regulator. The Bundesnetzagentur seems to accept the ruling and has demanded TSOs to return to the separate procurement of balancing capacity and energy. With this decision, a turbulent chapter on the German balancing markets finally comes to an end.

Take-aways for a healthy balancing market

The developments of the German market in recent years go a long way in showing what works and what does not when it comes to reserve power market design. What follows, are our take-aways.

Clearly, making a mixed price system work is difficult. We believe that a healthy reserve market separates the capacity and energy market. That capacity market needs to be open and competitive so that the costs for all grid users are reduced. The energy market needs to allow free pricing, which provides a strong incentive for all market parties to invest in good predictions and innovative portfolio management. Ideally, the energy market is also open to parties that can only commit flexible power on a short-term basis or during a few hours. These so-called free bids are put in the same merit order as the energy bids of market parties that were contracted in the reserve capacity market and hence provide additional downward price pressure on the balancing energy price.

To avoid exorbitant activation prices as seen in Germany in October 2017, the regulator can consider installing a price cap , but its height needs to be evaluated carefully. On the one hand, smaller players can suffer greatly from high imbalance prices. That could hinder new players to enter the market and hence reduces competition. On the other hand, a price cap distorts the market. In a future mainly powered with renewables, gas plants have fewer operating hours and have lower income in the wholesale markets. They show their value at moments of stress in the grid (with other words: when imbalance prices are high) and should be able to recover also investment costs in these moments. Keeping prices artificially low makes that impossible.

More to read

What about Belgium?

In Belgium, the national regulator and grid operator keep the capacity and energy markets separated and do not show any intention to consider the German mixed price system. They have also committed to transition the historically closed markets to an open and efficient system.

Already today, the market for tertiary reserves is open for all players and all technologies. The Transfer of Energy framework allows parties to valorise flexibility of assets within the balancing group of another BRP. Tenders are awarded based on capacity bids and activation prices to a large extent determine the order of activation. Of course, there are still inefficiencies, but market design is steadily being improved. The Belgian regulator CREG has adopted an activation price cap of 13 500 euros per MWh to avoid abuse of market power. Hence, an activation price as occurred in Germany in 2017 would not be possible here. So far, the price cap has never been reached.

Grid operator Elia is also working on opening the market for secondary reserve power. Of all balancing products, these reserves are the most important for Elia and represents the largest share in the procurement budget for reserve power. Therefore, there is good reason to make this market competitive rather sooner than later. Until then, we are stuck in the current closed market that is a legacy from the days of vertically integrated utilities. As a result, the secondary reserve market in Belgium is supplied by a small number of gas fired power plants.

This oligopoly, a natural result of the current market design, has some market distortive effects. Since the activation price for secondary reserves set the imbalance price (paid by the parties that cause a system imbalance) most of the time, the parties making up the oligopoly can control it to a large extent. The same companies take up such a big share of the Belgian market, that their own imbalance determines the whole system imbalance very often. They have therefore all reason to keep the imbalance prices low (see also info box). For them, it is a matter of optimizing income in the reserve market and imbalance penalties. This is a luxury other market participants don’t have.

This dynamic hampers a fully efficient balancing market in Belgium. The stimulus for market parties to manage their portfolios well is low and therefore the volumes traded on the intraday market are very limited. There is still a lot of room for Belgian market parties to manage their portfolio better, which would lead to less reserve power activations. The opening of the tertiary reserve market already showed that it reduces procurement costs for the grid operator and therefore their effort to open the secondary reserve market should be applauded – especially given the technical complexity of this product.

Conclusion

Our deep dive in the German market developments shows that healthy power exchanges and balancing markets can be reached by keeping reserve capacity and reserve energy markets separated and opening them up to as many market players as possible. The reserve energy market is preferably opened to free bids to increase competition. It could be protected against market manipulation by a sensibly set price cap. Belgium is on its way to such a market design, with grid operator Elia in the process of transitioning away from a system that historically favored large power plants and their owners to one where market parties large and small can participate on an equal basis.

Diseconomies of scale

The fact that the biggest Belgian utilities determine the system imbalance for most of the time gives way to a unique market feature. Having the largest portfolio in the market for once means being disadvantaged compared to smaller players: they are at the wrong side of the system imbalance most of the time. While normally large market parties enjoy the benefits of economies of scale, one could speak of diseconomies of scale here. The market parties in question mitigate this effect by controlling the secondary reserve activation prices. And of course… oligopolists have many other advantages that outweigh the effect described above.

More information and services

Elias De Keyser

Energy & Flexibility Expert

Jan de Decker

Co-founder & CEO Next Kraftwerke Belgium

Paul Kreutzkamp

Co-founder & CEO Next Kraftwerke Belgium